Tokenized government bond regulation has rapidly shifted from theory to practice, as sovereign issuers and global regulators grapple with the realities of integrating blockchain into the heart of public debt markets. As of December 2024, only $5 billion in tokenized Treasuries existed, a fractional share of the $27 trillion U. S. Treasury market, but this figure is rising fast as both demand and regulatory clarity accelerate. In 2025, the regulatory landscape for these digital securities is more dynamic than ever, with new frameworks emerging across major jurisdictions.

United States: Regulatory Momentum and New Federal Frameworks

The United States remains a focal point for tokenized bond innovation and compliance debate. In November 2024, the Commodity Futures Trading Commission’s (CFTC) Global Markets Advisory Committee endorsed expanding non-cash collateral via distributed ledger technology, a move that signals institutional acceptance and operational modernization for regulatory margin requirements. This step could pave the way for broader adoption of tokenized government bonds in collateral management and repo markets.

A pivotal moment arrived in July 2025 when Congress passed the "Corporate Guaranteed Notes and Regulatory Issuance Act" (GENIUS Act). While primarily targeting stablecoins, its provisions around reserve requirements and issuer obligations are expected to influence blockchain securities compliance more broadly, including tokenized government bonds. The Act’s alignment with existing securities law raises important questions about how digital representations of sovereign debt will be treated under U. S. federal oversight, especially as legal requirements remain in flux (source).

European Union: MiCA Ushers in Harmonized Regulation

The European Union has positioned itself at the forefront of tokenized bond legal framework development through its implementation of Markets in Crypto-Assets (MiCA) regulation in mid-2024. MiCA establishes a single regime across all EU member states for issuing, trading, and custodying asset-referenced tokens, including government bonds represented on blockchain networks. This harmonization provides much-needed legal certainty for institutional investors considering digital sovereign debt instruments.

SIFMA’s December 2024 study highlighted how these frameworks address long-standing limitations around settlement risk, transparency, and cross-border issuance (source). With MiCA now live, European institutions can launch regulated digital bonds accessible across multiple jurisdictions, potentially catalyzing secondary market liquidity while lowering operational costs.

US GENIUS Act vs. EU MiCA: Key Regulatory Differences

- Scope of Application: The GENIUS Act primarily targets stablecoins and reserve-backed digital assets, with indirect implications for tokenized government bonds, while MiCA explicitly covers asset-referenced tokens and provides a dedicated regime for tokenized securities, including government bonds.

- Regulatory Authority: In the US, the GENIUS Act establishes federal oversight, involving agencies like the SEC and CFTC, whereas MiCA centralizes supervision under the European Securities and Markets Authority (ESMA) and national competent authorities across EU member states.

- Issuer Requirements: The GENIUS Act mandates reserve requirements and disclosure obligations for stablecoin issuers, potentially influencing tokenized bond issuers. MiCA imposes strict authorization, governance, and transparency standards on all asset-referenced token issuers, including those offering tokenized government bonds.

- Cross-Border Harmonization: MiCA provides a passporting regime, allowing authorized issuers to operate across all EU member states. The GENIUS Act does not offer similar harmonization, leading to potential state-level regulatory variations within the US.

- Secondary Market and Investor Protections: MiCA sets out clear rules for secondary market trading, custody, and investor protection for tokenized government bonds. The GENIUS Act is less prescriptive on these aspects, relying on existing securities laws and agency guidance for secondary market activity.

Asia: Thailand’s G-Token Launch and Hong Kong’s LEAP Forward

Asia offers some of the most innovative approaches to tokenized government bond regulation. In May 2025, Thailand’s Securities and Exchange Commission introduced a dedicated framework for G-Tokens, digital tokens representing ownership in Thai government bonds. Scheduled to debut on secondary markets by July 2025 under SEC supervision, G-Tokens are designed to enhance investor protection while increasing transparency and access for retail and institutional participants alike (source).

Meanwhile, Hong Kong continues to assert its leadership with the June 2025 rollout of "Digital Asset Development Policy Declaration 2.0" and its LEAP framework. These initiatives prioritize real-world asset tokenization, including sovereign bonds, and offer policy support that could serve as a template for other Asian financial centers looking to modernize their capital markets infrastructure.

Despite these regulatory advances, the journey toward mainstream adoption of tokenized government bonds remains complex. Market participants must navigate a patchwork of compliance obligations, particularly where cross-border issuance and trading are involved. While frameworks like MiCA in the EU and the GENIUS Act in the US provide much-needed clarity, they also introduce new compliance burdens that require sophisticated legal and technological expertise.

One major challenge is ensuring interoperability between different blockchain networks and traditional financial market infrastructures. Without seamless integration, tokenized bonds risk remaining siloed, limiting their potential to enhance liquidity or streamline settlement cycles. Another hurdle is investor education, both institutional and retail investors need to understand the nuances of digital custody, smart contract risks, and redemption processes unique to blockchain-based securities.

Key Considerations for Global Investors

For global investors eyeing this emerging asset class, several considerations stand out:

Essential Due Diligence Steps for Tokenized Government Bonds

- Verify Regulatory Compliance in Relevant Jurisdictions: Confirm that the tokenized government bonds are issued under clear regulatory frameworks, such as the EU’s MiCA regulation, the U.S. GENIUS Act, or Thailand’s G-Token framework. Ensure the issuer and platform comply with all local and cross-border requirements.

- Assess the Issuer’s Track Record and Reputation: Investigate the government or authorized entity issuing the bonds, their history with digital assets, and any prior tokenization projects. Look for established issuers like the Thai Government (G-Token) or Hong Kong’s LEAP framework participants.

- Review Custody and Settlement Arrangements: Examine how digital tokens are held and settled. Ensure the platform uses secure, regulated custodians and robust settlement mechanisms, as required by frameworks such as MiCA and Hong Kong’s LEAP.

- Evaluate Secondary Market Liquidity: Analyze the availability and depth of secondary markets for tokenized government bonds, including platforms authorized under EU MiCA or Thailand’s SEC. Confirm that secondary trading is permitted and supported by regulated exchanges.

- Understand Technology Infrastructure and Security: Assess the underlying blockchain technology, smart contract audit status, and cybersecurity measures. Prefer platforms with transparent security protocols and third-party audits, as highlighted in BIS and Shin (2024) reports.

- Confirm Redemption and Settlement Processes: Ensure redemption at par and timely settlement, as required by FCA rules and other regulatory standards. Review the issuer’s procedures for handling redemption requests and investor payouts.

- Monitor Ongoing Regulatory Developments: Stay updated on evolving regulations from bodies such as the CFTC, SEC, and EU authorities. Regulatory landscapes for tokenized assets are rapidly changing and may impact investment risks and opportunities.

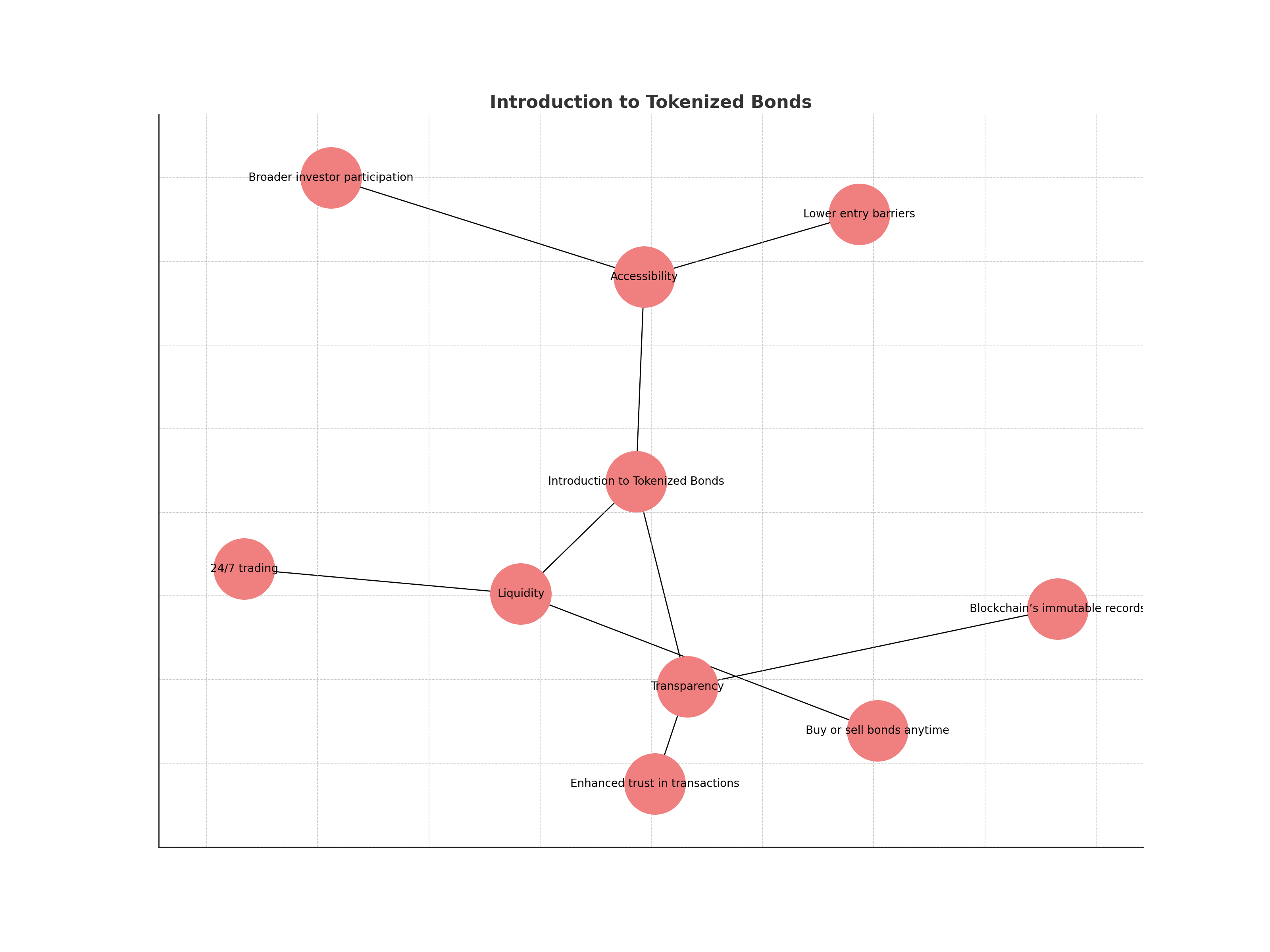

First, robust due diligence on both technology providers and regulatory compliance is essential. Investors should scrutinize whether tokenized bond platforms adhere to local securities laws and offer sufficient safeguards against operational risk. Second, attention must be paid to secondary market liquidity, while frameworks like Thailand’s G-Token aim to foster active trading venues, most markets remain nascent compared to traditional bond exchanges.

Third, questions around data privacy, cyber resilience, and dispute resolution mechanisms loom large as more sovereign issuers experiment with public or permissioned blockchains. The promise of 24/7 settlement and fractional ownership must be weighed against evolving standards for investor protection and transparency.

Looking Ahead: Models for Future Regulation

The success of pilot programs such as Thailand’s G-Token and Hong Kong’s LEAP framework will likely shape future regulatory approaches worldwide. As more jurisdictions observe their outcomes, especially regarding investor uptake and risk management, expect a wave of policy adaptation. The CFTC’s endorsement of distributed ledger collateral in the US may signal an eventual convergence between traditional regulatory goals and digital innovation.

Ultimately, achieving scale in tokenized government bonds will depend on continued collaboration between regulators, issuers, technology providers, and market participants. The current $5 billion in tokenized Treasuries marks only an initial step; as legal frameworks mature globally, this figure could grow exponentially, reshaping fixed-income investing for decades to come.

No comments yet. Be the first to share your thoughts!