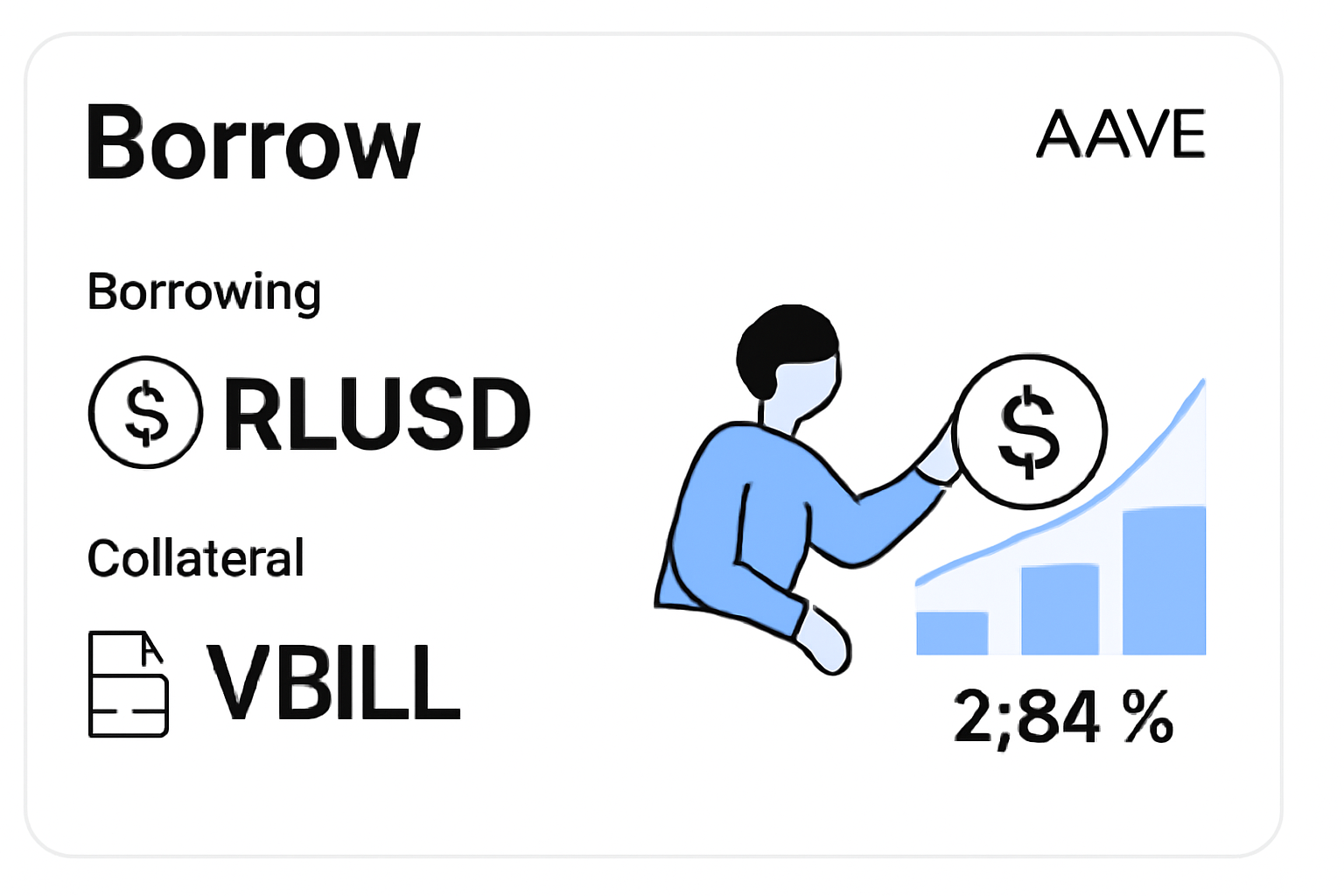

VanEck VBILL Tokenized Treasury Fund on Aave Horizon: Collateral Strategies and Yields 2025

In the evolving landscape of decentralized finance, the integration of VanEck’s VBILL tokenized Treasury fund into Aave’s Horizon RWA market stands out as a thoughtful bridge between traditional fixed-income assets and blockchain innovation. Launched in November 2025, this move allows institutional investors to use VBILL, backed by U. S. Treasury securities, as collateral, unlocking liquidity while preserving the safety of government debt. With current liquidity at $9.17 million, a 7-day yield of 3.93%, and RLUSD borrowing costs around 2.84%, VBILL offers a compelling entry point for tokenized treasury collateral on Aave. This development not only enhances Aave Horizon RWA market participation but also signals maturing infrastructure for tokenized US Treasuries in DeFi 2025.

Understanding VBILL’s Role in Horizon’s Ecosystem

VanEck’s VBILL represents a tokenized fund that holds short-term U. S. Treasuries, delivering stable yields through blockchain wrappers. Its addition to Aave Horizon, a permissioned marketplace launched in August 2025, expands the platform’s total value locked toward $590 million. Institutions can now deposit VBILL tokens, tapping into DeFi lending without selling their Treasury exposure. This setup appeals to portfolio managers like myself, who prioritize risk-adjusted returns amid regulatory clarity and infrastructure growth seen in November 2025 recaps.

The fund’s appeal lies in its yield profile: that steady 3.93% over seven days outpaces many traditional alternatives when leveraged thoughtfully. Borrowing against it at 2.84% creates a positive carry, but success hinges on disciplined position sizing and market vigilance.

VBILL Key Metrics on Aave Horizon

| Metric | Value |

|---|---|

| Liquidity 💰 | $9.17M |

| 7-day Yield 📈 | 3.93% |

| RLUSD Borrow Rate 💳 | 2.84% |

| Looped Yield Potential 🔄 | ~5.5% |

| Horizon TVL 🌐 | nearing $590M |

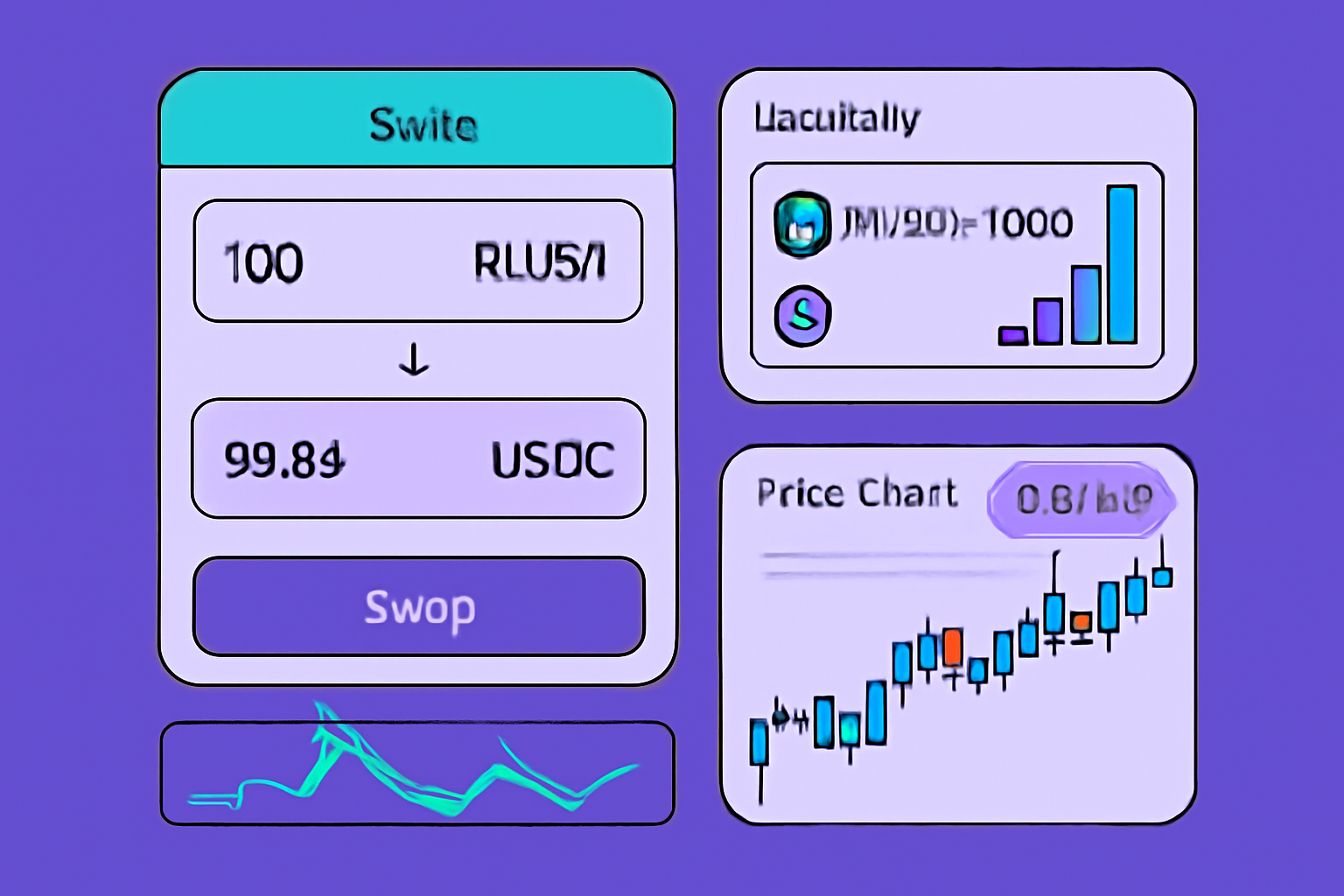

Mastering Collateral Strategies for VBILL Yield Optimization

VBILL yield strategies shine brightest through leveraged looping, a technique that amplifies base returns without excessive speculation. By depositing VBILL as collateral, borrowing RLUSD, converting to USDC, and repurchasing more VBILL, users can compound exposure. Estimates place amplified yields around 5.5%, assuming stable rates and no major volatility. This isn’t gambling; it’s a calculated enhancement for long-term holders, reminiscent of sustainable finance principles where patience meets opportunity.

Yet, I advise caution: monitor the spread between VBILL’s 3.93% yield and the 2.84% borrow cost closely. A narrowing gap erodes profitability, underscoring the need for dynamic risk management in VanEck VBILL Aave deployments.

Unlocking Amplified Yields: VBILL Leveraged Loop on Aave Horizon

Chainlink and Securitize: The Pillars of Reliable Pricing

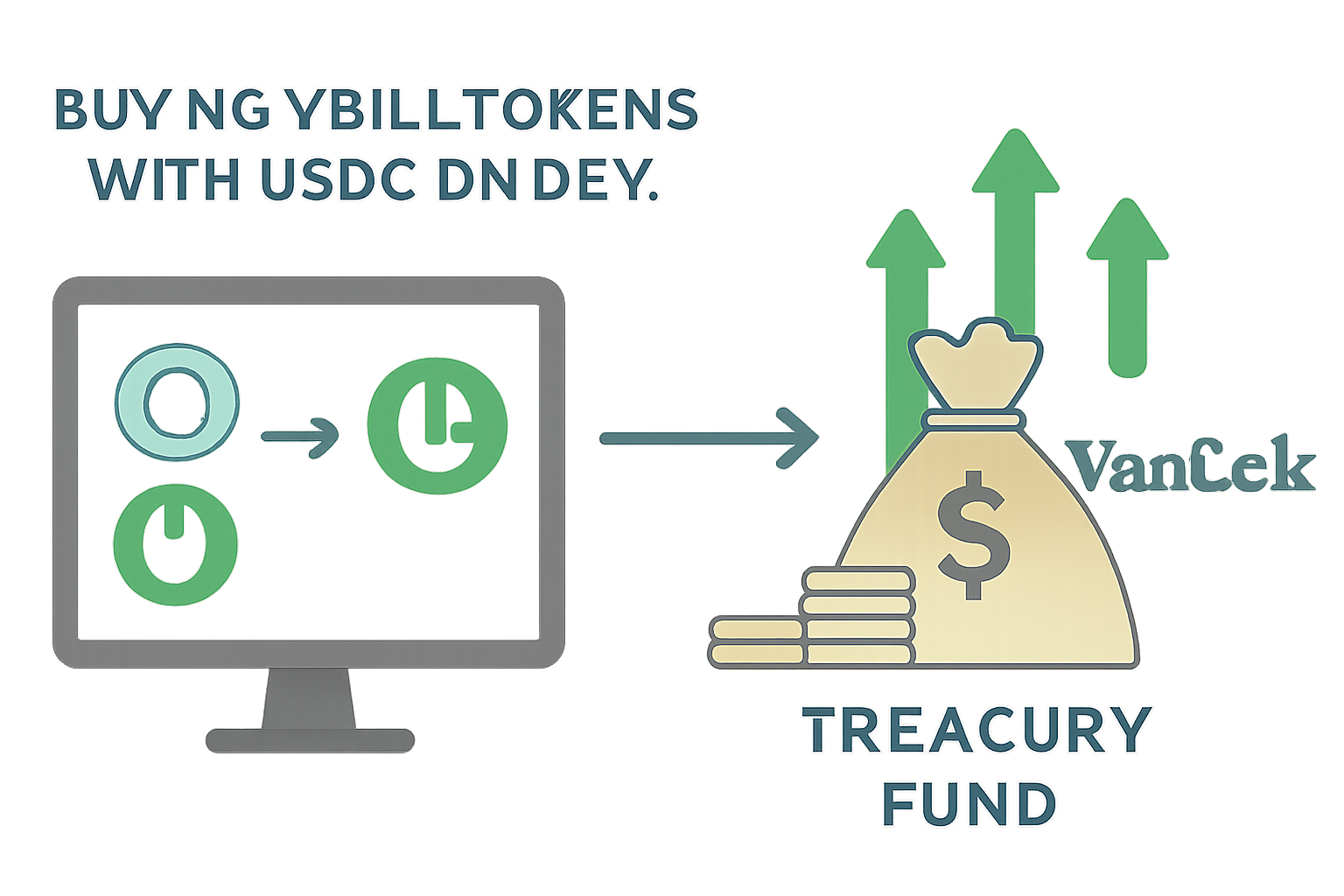

Behind VBILL’s seamless operation lies robust technology. Chainlink’s NAVLink oracle delivers real-time, tamper-proof net asset value data, ensuring collateral valuations reflect true Treasury backing. Securitize’s platform handles compliant issuance, with upcoming Trusted Single Source Oracle enhancements promising even greater verification. This stack mitigates common DeFi pitfalls like oracle failures, fostering trust for conservative investors eyeing RWA growth from $13 billion in late 2024 to $35.8 billion in 2025.

In my view, these integrations exemplify macro trends: tokenized assets aren’t just hype; they’re practical tools for liquidity and transparency in fixed-income portfolios.

While the technological backbone inspires confidence, no strategy operates in a vacuum. The real test comes in navigating volatility and economic shifts that could test even the sturdiest collateral setups.

Navigating Risks in VBILL Collateral Deployments

In leveraging tokenized treasury collateral on Aave, the spread between VBILL’s 3.93% 7-day yield and RLUSD’s 2.84% borrow rate forms the foundation of profitability. A compression here, say from shifting Fed policy or rising DeFi demand, could flip positive carry into a drag. More critically, VBILL trades near $1 parity with its Treasury holdings; any deviation below that threshold risks liquidation cascades, especially in looped positions pushing loan-to-value ratios. I’ve seen similar setups in traditional leveraged bond funds falter during rate surprises, reinforcing why VBILL yield strategies demand ongoing vigilance over blind automation.

SmartMoney protocols like LlamaGuard add safeguards, but they can’t eliminate tail risks such as oracle disruptions or black swan events. For institutions, this means setting conservative LTV limits, perhaps 60-70%, and stress-testing against yield drops to 3% or borrow spikes above 3.5%. Patience pays; rushing into max leverage invites regret.

VBILL Risk Assessment

| Metric | Value | Details |

|---|---|---|

| Yield Spread | 1.09% (3.93%-2.84%) | VBILL 7-day yield minus RLUSD borrowing cost |

| Liquidation Threshold | ~$1 | Price drop below peg risks leveraged position liquidation |

| Max Recommended LTV | 70% | Suggested max loan-to-value to mitigate risks |

| Potential Looped Yield | 5.5% | Estimated yield from deposit-borrow-loop strategy |

| Key Monitor | Fed Rate Changes | Monitor for impacts on yields and spreads |

Leveraged Loops in Action: A Practical Breakdown

Let’s demystify the looped yield mechanic that can nudge returns toward 5.5%. Start with $1 million in VBILL deposited into Aave Horizon. Borrow up to 80% in RLUSD at 2.84%, netting $800,000. Swap to USDC via integrated DEXs, repurchase VBILL at prevailing NAV, and redeposit. Each cycle compounds exposure, but cap iterations at three to four to avoid overextension. Chainlink’s pricing keeps this honest, validating every step against real-time Treasury values.

This isn’t for novices; it suits seasoned allocators blending DeFi with core fixed-income sleeves. In my portfolios, we layer such tactics atop unlevered VBILL holdings, targeting 4-6% net yields while hedging duration risk. The beauty lies in reversibility: unwind anytime without tax events plaguing traditional margin calls.

2025 Market Momentum: RWA Expansion and Institutional Flows

Aave Horizon’s TVL push past $540 million, en route to $590 million, mirrors broader RWA surges from $13 billion in late 2024 to $35.8 billion this year. VBILL’s $9.17 million liquidity anchors this growth, drawing funds from BlackRock’s BUIDL peers and new entrants. November 2025 recaps highlight regulatory tailwinds, like clearer SEC nods on tokenized funds, accelerating what was once fringe experimentation into mainstream collateral.

Zoom out, and Aave Horizon RWA market dynamics echo tokenized U. S. Treasuries hitting multi-billion caps across platforms. For context, see how DeFi collateral pools have evolved alongside Bybit integrations at this overview. Institutions now command over half of RWA TVL, per RedStone reports, validating tokenized US Treasuries DeFi 2025 as a staple, not a side bet.

Looking ahead, expect TSSO upgrades and multi-chain expansions to deepen VBILL’s utility. Yield-bearing stablecoins may soon pair directly, squeezing borrow costs further. As a portfolio manager focused on sustainable macro plays, I see VBILL on Aave as a linchpin for hybrid strategies: earn Treasury safety, amplify via DeFi, and sleep soundly knowing blockchain adds verifiable transparency traditional brokers can’t match.

Deploy thoughtfully, and these tools align performance with the fixed-income future we all anticipate.